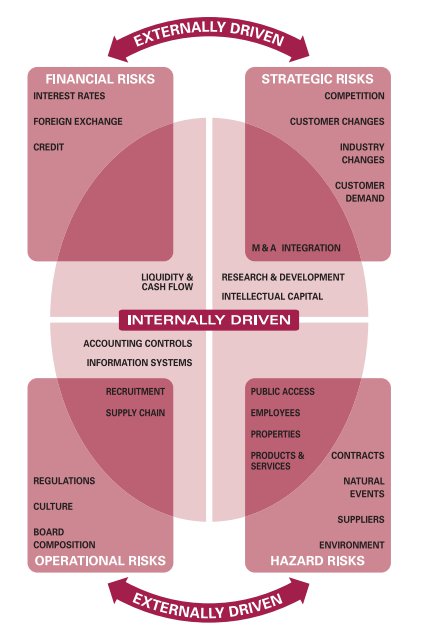

Many risk types impact both financial and nonfinancial outcomes. However, the connection between cause, event and impact is more loosely defined for nonfinancial risks.

Financial risk is the possibility that a financing entity will not be able to meet its debt obligations. Examples include auto loans, mortgages and credit cards.

Asset-backed risk

Financial risks are the consequences of unforeseen untoward events. They can be measured in monetary terms and often lead to large losses. They can be either systematic or non-systematic. For example, an industrial or road accident can lead to medical costs or Court awards, and the death of a breadwinner in a family can result in a loss of income for the rest of the family. All these are examples of financial risk, which are covered by insurance policies.

The most common types of financial risk are market risk, credit risk and liquidity risk. Market risk is caused by fluctuations in market parameters like interest rates, stock indices and exchange rates. Managing this type of risk involves monitoring the fluctuations and controlling them within an agreed limit.

Credit risk is a risk that a customer or counter-party does not meet its obligations in relation to lending/trading/hedging/settlement activities. It can be due to unforeseen circumstances, such as bankruptcy, resignation or insolvency. Moreover, the failure of a government to pay its debts also constitutes financial risk for investors/stakeholders. This is because it may cause a global crisis and affect the monetary status of the whole marketplace. Managing this type of risk requires a thorough understanding of the business model, including its assumptions and their impact. The governance board, company management and financial analysts should be aware of the importance of a holistic approach to risk management.

Cyberattacks

Cyberattacks are a growing threat that can affect all sectors. Many businesses, including retailers and banks, are targets for malicious cybercriminals seeking customer data or corporate espionage. Medical services and government entities are also vulnerable to cyberattacks. These threats are becoming more common and require increased spending on cybersecurity solutions.

The attack on telecommunication infrastructures is one example of how cyberattacks can cause systemic damage. Currently, most telecommunications networks use Internet connectivity, which makes it easier to attack. The attack could reroute the network or cause it to slow down. This could lead to loss of revenue and reputational damage. In addition, the attack could expose confidential information or create a security breach.

Although many governments do not admit to launching cyberattacks, they are increasingly responsible for this type of warfare. For instance, US and UK intelligence agencies are thought to be behind the Stuxnet malware that attacked Iran’s nuclear facilities in 2010. Moreover, Russian groups with links to the country’s government are alleged to have conducted a series of attacks on Estonia’s parliament, banks, and TV stations during 2007 as part of an ongoing dispute over Soviet war graves.

Nonfinancial risks are difficult to predict, as they are based on evolving business models and changing customer expectations. Unlike credit and market risk, which can be evaluated from historical data, these risks require iterative process improvement and a more robust risk-management framework. This is why it is important for companies to focus on building a strong first line of defense.

Reputational risk

Reputational risk is the threat that a bank will lose consumer and stakeholder trust because of an event that is outside its control. It’s less predictable and harder to quantify than other types of risk, but it can have a major impact on a company’s bottom line. Banks that have a reputational risk management plan in place can better protect themselves from this type of risk.

Nonfinancial risks are more difficult to manage than financial risks because they don’t typically involve financial decisions. In banking, these risks include operational, reputational, and strategic risks. These risks have a wider range of root causes, events, and impacts, making it harder to find a direct link between them. Additionally, there is often less risk data available for these risks, which makes them more qualitative in nature.

This is especially true for the operational and reputational risks. While industrial corporates have begun to develop frameworks for managing these risks, banks have had a more difficult time. As a result, there is still a need for a unified methodology that can help banks better identify and manage these risks. The current amendment to MaRisk in BTR 4 requires that these risks be integrated into a risk management framework, and this is an important step forward. However, it’s important to remember that risk models cannot address all risks. They must be balanced to achieve the best results.

Liquidity risk

Liquidity risk is the danger that an asset will not be easily sold for cash in a short period of time without impacting its market price. This can cause an entity to have a negative financial outcome, such as losing money or income. Financial institutions often undergo stress tests to assess their liquidity. This is a risk that should be considered along with credit risk and operational risks.

This is a risk that a firm may not be able to meet its financial obligations, such as loan payments or supplier payments, due to a lack of cash on hand. To mitigate this risk, a business can set up lines of credit or an emergency fund. Another way to mitigate this risk is by purchasing insurance or creating contracts that limit liability.

A common measure of liquidity risk is the liquidity gap, which measures the difference between a financial institution’s liquid assets and its volatile liabilities. However, this metric can be misleading, as it only considers changes in funding costs and assumes that all maturities are affected equally.

Another type of liquidity risk is market liquidity risk, which occurs when a company cannot sell an illiquid asset at short notice. This can lead to a loss of income, especially if the asset is highly valued. A recent example of this was the failure of Toys “R” Us, which was bought in 2005 by private equity firms KKR and Bain Capital.