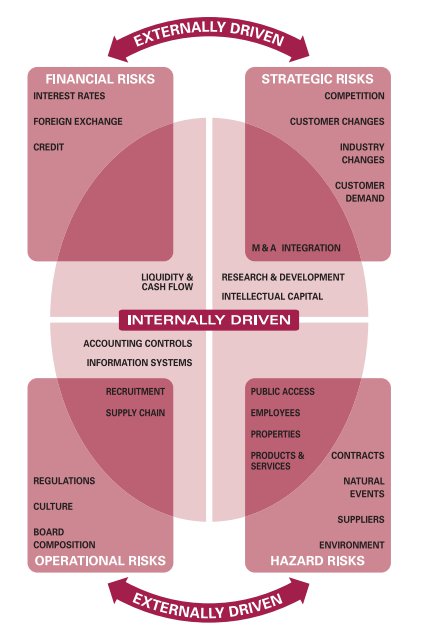

Financial institutions face a number of different types of risk. Some of the most common risks are credit risk, liquidity risk, and operational risk.

Credit risk is the risk that borrowers will default on their debts. When this occurs, investors lose out on both principal and interest payments. It also leads to increased costs for loan collection.

Credit Risk

Credit risk is the risk that a lending institution will not be paid back for money it loans to businesses or individuals. Lenders go to great lengths to assess an individual’s or business’ ability to repay debt and mitigate the chance of loan loss. They may perform extensive financial investigations, use a credit score to rank potential borrowers, require security over assets, take out insurance or on-sell the debt to another party.

When a business or individual fails to pay back their debt, the lender incurs losses in both principal and interest. This also disrupts cash flow and increases collection costs. Banks must carefully manage their loan book to avoid credit losses, and this is often done by limiting concentration risk in the form of limits on how much can be lent to a single borrower or even a particular industry sector.

In addition to lending, banks can also face credit risk in other activities, such as accepting depositors, making trade financing arrangements and extending commitments and guarantees. Generally, these are not as material to the banking book as loans, but they still expose a bank to the possibility of losing money. Banks are required to provide for these exposures in their accounting operating statements through provisions and write-offs, which represent a significant component of most banks’ risk-weighted assets.

Market Risk

Market risk refers to the potential loss of investment capital resulting from price volatility in markets to which a financial institution is exposed. These price fluctuations often occur due to unanticipated movements in factors that commonly affect the performance of financial markets, such as economic conditions and political events. It is important to identify these risks and manage them effectively to maximize returns and minimize exposure to losses.

A key source of market risk for financial institutions is interest rate risk, which arises from a combination of fixed-rate assets and liabilities on their balance sheets. When interest rates rise, the value of fixed-rate instruments such as bonds decreases and when rates fall the inverse happens. This is largely driven by monetary policy measures undertaken by central banks and inflation expectations.

Financial institutions use models to help them understand the price sensitivity of their investments in response to changes in these factors. These models provide critical information needed to make sound decisions and determine appropriate levels of market risk.

The models used to calculate risk can include statistical methods such as Value at Risk (VaR), Conditional Value at Risk (CVaR) and risk-adjusted performance ratios like Sharpe, Sortino, Treynor and the like. The models can also incorporate factors that are more qualitative in nature, such as liquidity risk and commodity risk.

Liquidity Risk

Liquidity risk is the risk of a financial institution’s inability to meet payment obligations as liabilities fall due. This can occur on an individual bank basis or on a systemic level. Banks can mitigate liquidity risks by assessing their current and future cash flow needs on a daily basis, stress testing and using asset-liability management techniques. Liquidity risk can be separated into two categories: Market liquidity risk and funding liquidity risk.

The former occurs when an investor, business or financial institution is unable to quickly sell an illiquid asset in order to fund debt repayments. This is generally the result of a lack of buyers or an economic shift that depletes demand for the particular commodity.

In a banking context, this type of liquidity risk can be exacerbated when a bank is unable to provide enough cash to customers who want to withdraw funds. This can lead to a snowball effect where other customers become more hesitant to use the bank because they don’t trust it with their money.

Liquidity risk tends to compound other types of risk, such as market and credit. It’s important for trading organizations to avoid illiquid assets and have access to sufficient liquidity to off-set positions at short notice, especially during times of economic stress. In addition, they should minimize the amount of debt on their balance sheet and optimize their net working capital and existing credit facilities.

Operational Risk

Financial institutions must deal with operational risk, which is the risk that internal systems or people fail. This type of risk is very different from the more abstract, systemic risks that are inherent in a market or industry, and it is often difficult to identify and measure.

Human error is a key component of operational risk, which includes losses due to data entry errors, accounting mistakes, failed mandatory reporting and outright fraud. It can also include the chance that a company’s technology infrastructure is not as secure or reliable as its competitors’. This is especially true in an increasingly digitized world, where many financial services firms rely on third-party IT providers for core banking and other vital systems.

The loss potential from these weaknesses is huge. Not only can the resulting errors lead to fines from regulators, they can also damage a firm’s reputation and undermine customer confidence. Many of the headline-generating bank scandals over the past decade stemmed from operational risk issues.

The good news is that the financial industry has made great strides in improving operational risk management, which will help it manage this type of risk more effectively going forward. However, the risks remain a major concern and are likely to continue to grow. It’s essential that banks recognize these risks, evaluate their exposure to them and mitigate them wherever possible.